Raising Fund I – III

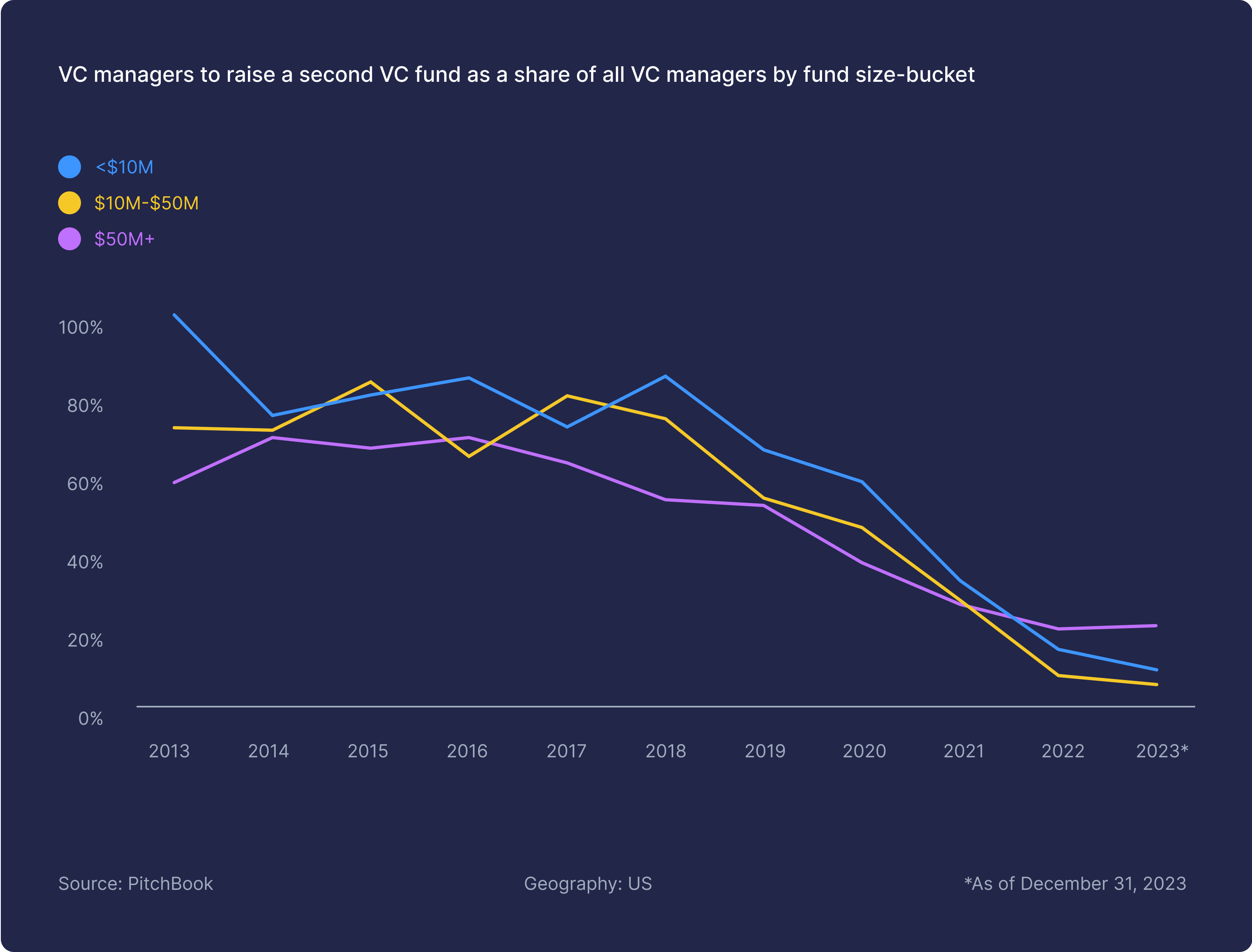

The adage that the first fund is the most challenging to raise has often been heard. However, the stark reality as also revealed in recent data by Pitchbook illustrates that the second (and third) fund present an even greater challenge as many LPs will expect to see mark-ups and you’re juggling running your firm at the same time as you’re on the fundraise trail.

These years, however, that dynamic has only been extenuated as many Fund I’s were raised at a time when new VC LPs had overly grand return expectations where many started to talk about 5x being the new benchmark for a pre/seed fund and many VCs followed suit in their promises. Mix this with the general loss in trust and the other effects discussed in the past section including the fact that many new funds deployed the majority of their capital at the top of the market and you have a cocktail from hell. Or rather, you have the below chart recently published by PitchBook.

Through the years, we’ve spoken to numerous VCs and LPs about how emerging managers can best demonstrate performance through fund I, II and III. In the following, we’ve collected our learnings as well as conducted four dedicated LP interviews to cover the topic in detail.

Demonstrating performance as an emerging manager

Raising European venture capital funds, particularly through the critical early stages of a venture capital firm’s lifecycle, is an intricate dance of strategic positioning, narrative crafting, and relationship building with LPs. Emerging managers, navigating their journey from Fund I through to Fund III, face evolving challenges and opportunities at each juncture. The insights gleaned from leading European LPs, such as Ertan Can, Founding Managing Partner of Multiple Capital, Stepfan Heller, Founding managing partner of AQVC, and David Dana, head of VC investments at EIF, provide some important learnings about what they as institutional LPs look for emerging managers when considering Fund I, II and III.

Below, we feature first the core learnings about how LPs diligence emerging fund managers and secondly each individual interview.

Fund I

Foundations and narrative

The process of due diligence conducted by LPs on Fund I initiatives, particularly when evaluating the track record and performance potential of first-time fund managers, is intricate and multifaceted. LPs employ a variety of methods to scrutinise the viability and strategic positioning of new funds, going beyond the surface to assess the underlying potential for success. Here are key elements and practices highlighted in the transcripts that LPs focus on during their due diligence process:

01 Deep dive into investment thesis coherence and market fit

LPs critically evaluate the investment thesis of the fund, focusing on its coherence, differentiation and alignment with current market opportunities. They assess how well the fund’s strategy addresses the unmet needs within the venture ecosystem, the scalability of the targeted sectors, and the potential for the fund to carve out a unique position in the market.

02 Assessment of team composition and synergies

The collective experience, expertise, and synergy of the fund management team will be scrutinised. LPs look for complementary skill sets among team members that cover critical aspects of venture investing, including deal sourcing, due diligence, portfolio management, and exit strategies. The presence of a well-rounded team with a history of collaboration and success in previous ventures or roles adds to the fund’s credibility.

03 Evaluation of proprietary deal flow sources

Access to a robust and proprietary deal flow is a critical factor for the success of any venture fund. LPs examine the fund manager’s network, partnerships, and strategies for sourcing deals. The ability to tap into undiscovered or under leveraged markets, or to bring novel technologies or business models to the forefront, is particularly valued.

04 Proof of concept through track records or analogous achievements

While first-time fund managers may not have a direct track record in fund management, LPs look for proof of concept through analogous achievements. This could include success in angel investing, leadership in high-growth startups, or significant operational roles in industry sectors relevant to the fund’s focus. Evidence of past success that can be translated into venture investing acumen is thoroughly evaluated.

05 Rigorous reference checks

LPs conduct extensive reference checks, reaching out to co-investors, entrepreneurs, and industry experts who have interacted with the fund managers in various capacities. These references can provide insight into the manager’s operational competence, investment judgement, ethical standards and ability to add value to portfolio companies beyond capital.

06 Detailed financial and risk analysis

A comprehensive financial analysis is undertaken to understand the fund’s expected return profile, fee structure, and alignment of interest through carried interest mechanisms. Additionally, LPs assess the risk management strategies of the fund, including diversification approaches, sector-specific risks, and the fund’s capacity to navigate economic downturns.

07 Commitment and skin in the game

LPs value a significant commitment from fund managers, often referred to as “skin in the game”. This commitment, demonstrated through substantial personal investment in the fund, aligns the interests of the managers with those of the LPs and serves as a testament to the manager’s confidence in their strategy.

By leveraging these thorough due diligence processes, LPs aim to mitigate the inherent risks of investing in first-time funds while uncovering potential opportunities for exceptional returns. This meticulous approach ensures that investments are made in fund managers who not only possess a promising strategy and vision but also have the capability, network, and operational excellence to execute on that vision effectively.

Fund II

Evolution, execution and expansion

The due diligence process for Fund II by LPs reflects an evolution from the scrutiny applied to first-time funds, incorporating lessons learned and successes from Fund I while addressing the unique challenges and opportunities of managing a subsequent fund. In Fund II, LPs are particularly focused on how the general partners have leveraged their initial experiences, scaled their operations, and refined their investment strategies. The evaluation of Fund II encompasses several key areas:

01 Performance analysis of Fund I

A critical aspect of due diligence for Fund II involves a deep dive into the performance metrics of Fund I. LPs meticulously analyse the realised and unrealised returns, exit strategies, and portfolio company growth metrics. This analysis helps assess the GPs’ investment acumen, market timing, and ability to generate alpha. Special attention is given to the lessons learned from investments that did not perform as expected, and how these lessons have informed the strategy for Fund II.

02 Evolution of investment thesis

LPs examine how the investment thesis has evolved from Fund I to Fund II, seeking clarity on whether the shift reflects a response to market dynamics, insights gained from prior investments, or a strategic pivot based on the team’s strengths. The consistency and rationale behind the evolution of the thesis are evaluated to ensure that Fund II is positioned to capitalise on current and emerging market opportunities.

03 Scalability and operational maturity

With Fund II, LPs expect a higher level of operational maturity and scalability in fund management practices. This includes enhanced deal sourcing mechanisms, portfolio support services, and back-office operations. The ability of the GPs to scale their operations effectively, incorporating sophisticated tools and processes for managing a larger and potentially more complex portfolio, is a key focus area.

04 Expansion of the team and network

The growth and diversification of the GP team are crucial elements in the due diligence of Fund II. LPs assess the addition of new team members, focusing on their backgrounds, expertise, and how they complement the existing team’s strengths. An expanded network, including strategic partnerships and advisory boards that can provide value-add to portfolio companies, is also a significant consideration.

05 Portfolio construction and risk management

The approach to portfolio construction for Fund II is scrutinised with LPs looking for a well-defined strategy that balances risk and return across sectors, stages, and geographies. The risk management framework, especially how it has been adapted or strengthened based on experiences from Fund I, is equally evaluated.

06 Continued alignment of interests

The alignment of interests between GPs and LPs remains a fundamental concern. LPs review the fee structures, carried interest arrangements, and the GPs own investments in Fund II to ensure that incentives are correctly aligned for long-term value creation.

07 Enhanced reporting and communication

The quality of reporting and communication from Fund I serves as a benchmark for expectations with Fund II. LPs value transparency, regular updates, and insightful analysis on portfolio performance and market trends. The ability of GPs to maintain an open and informative communication channel is considered indicative of their commitment to partnership and governance excellence.

When conducting due diligence for Fund II, LPs leverage a blend of quantitative metrics and qualitative assessments to form a holistic view of the fund’s potential. The focus is not only on the past performance but also on the strategic adjustments, team evolution and operational enhancements that signal the fund’s capacity to adapt and thrive in a dynamic venture capital environment.

Fund III

Establishing a track record and scaling operations

Due diligence on Fund III for LPs marks a significant phase where the focus intensively shifts towards assessing maturity, sustainability, and strategic foresight of the venture capital fund’s operations and investment philosophy. By this stage, LPs are not merely looking at past performance as a predictor of future success but are also keenly evaluating the fund’s ability to innovate, its market position, and the robustness of its ecosystem. This nuanced approach towards due diligence encompasses several critical dimensions:

01 Track record and performance continuity

The performance of both Fund I and Fund II is scrutinised to assess not just the returns but the consistency and sustainability of performance across market cycles. LPs are particularly interested in understanding how the fund has navigated market downturns, the resilience of its portfolio companies, and the GP’s ability to execute successful exits even in challenging conditions.

02 Strategic positioning and market insight

By Fund III, LPs expect the GPs to have developed a deep market insight and a clear strategic positioning that differentiates them from competitors. This involves a thorough examination of the fund’s investment thesis, sector focus, and geographic strategy, ensuring they are not only relevant to the current market dynamics but are also forward-looking, anticipating future trends and disruptions.

03 Operational excellence and scalability

The operational maturity of the fund is a critical area of due diligence for Fund III. LPs delve into the fund’s infrastructure, technology adoption, and process efficiencies to evaluate how these elements support scalability. The focus is on the fund’s ability to manage a growing portfolio without compromising on the quality of support and engagement with its investments.

04 Ecosystem development and value addition

Fund III due diligence also involves evaluating the ecosystem that the fund has built around its portfolio companies, including co-investors, strategic partners, and advisory networks. LPs look for evidence of how this ecosystem delivers tangible value to portfolio companies, facilitating their growth, market expansion, and operational efficiency.

05 Team dynamics and evolution

The composition, stability, and evolution of the management team receive detailed attention. LPs are interested in how the team has expanded, the addition of new skill sets and experiences, and how succession planning and leadership development are managed. The continuity of the team and its alignment around the fund’s vision are seen as indicators of the fund’s stability and long-term potential.

06 Environmental, social, and governance (ESG) integration

By the time of Fund III, the integration of ESG principles into the investment process is often a significant area of focus. LPs assess the fund’s commitment to ESG, not as a tickbox exercise but as a core part of the investment strategy that aligns with long-term value creation and risk mitigation.

07 Innovation and adaptability

Finally, LPs evaluate the fund’s capacity for innovation and adaptability. This includes the fund’s approach to emerging technologies, new business models, and shifts in consumer behaviour. The ability to adapt investment strategies, explore new sectors, and pivot in response to market changes is a key determinant of a fund’s long-term success.

For Fund III, the due diligence process is as much about confirming the solid foundations and successes of the past as it is about evaluating the fund’s preparedness for future challenges and opportunities. LPs use this opportunity to deepen their understanding of the fund’s strategic direction, operational robustness, and the potential for sustained value creation in a dynamic and competitive environment.

Key learnings

Value proposition

Before performance can even be considered, David Dana emphasises the unique value proposition of the emerging manager. What differentiating element or added value can they bring to the market that isn’t already covered by existing players?

Technical and operational expertise

Emerging managers should have a team with strong technical and operational expertise, particularly in deep tech segments like AI, space tech, quantum, and semiconductors. This isn’t just about bringing capital to entrepreneurs but also significant added value.

VC management expertise

Besides technical knowledge, it’s crucial for the team to have VC management expertise. Understanding the VC market, how to manage a fund, and interact with investors and LPs is a must.

Track record and angel investments

For first-time funds, a concrete, extensive track record might not be available. Instead, David Dana looks for evidence of wise angel investments or involvement in successful ventures that can serve as indicators of the team’s ability to source and select promising companies.

Assessing business angel investments

Given the early-stage nature of many investments, particularly in deep tech, Dana doesn’t expect to see DPI (Distributions to Paid-In capital). Instead, he evaluates the company’s progress and potential based on KPIs like revenue and growth rate.

Case-by-case analysis of track record

There is no “magic number” of investments that defines success. Dana conducts a detailed analysis of each company in the portfolio, assessing the co-investors, attraction, expected KPIs, and the company’s development since the time of investment.

Fund model

Dana insists on a realistic and well-constructed fund model. He looks for experience with full investment cycles and at least one exit, even if it’s not profitable. Understanding the technicalities of running a VC fund is essential, and the team must show they can follow through on their strategy and promises to LPs.

Importance of demonstrating VC understanding

Dana underlines the importance of demonstrating a thorough understanding of VC principles. Teams must be aware of the basic assumptions of VC and should be able to explain any deviations from these norms in their approach.

Substance over style in proposals

Emerging managers must ensure that their pitch decks and proposals are well thought out and substantive. A poorly constructed fund model or lack of a clear strategy can lead to immediate dismissal.

The role of differentiation

Lastly, emerging managers with limited track records must clearly articulate their raison d’être. They must convince potential investors like the EIF of their potential for higher returns and their unique position in the market.

Key learnings

Acceptance of power law

There is an acknowledgment that not all VC funds, especially first-time funds, will be out performers. The expectation is that a minority, perhaps 10 to 20 percent, will become outlier funds, with the remainder performing average or below average.

Role of randomness

Ertan Can notes the randomness in fund success, citing that outliers in his experience have come from unexpected places, suggesting a belief in the potential rather than the certainty of each fund being a standout.

Assessment beyond immediate performance

The transition from a first to a second fund often does not provide sufficient time to demonstrate real performance in terms of markups or DPI. Early successes or markups are seen as unsustainable for predicting future performance.

Consistency and focus

Ertan values the consistency of the emerging manager with their initial strategy and approach. He looks favorably upon GPs who remain focused on their initial thesis and do not chase current market hypes or trends without a well-thought-out reason for any strategic shifts.

Networking and co-investor quality

The ability of a GP to build a network, attract follow-on investments from reputable names, and be invited to competitive rounds is viewed as more important than early performance metrics.

Entry valuations as KPIs

An important KPI for Ertan is the range of entry valuations a fund manager secures. Investing at lower entry valuations, indicative of conviction and an earlier investment stage, is preferred over higher entry valuations that might follow market signals or competitiveness.

Brand building and recognition

Building a recognisable brand and becoming the go-to GP in a specific region, vertical, or niche is deemed more crucial than first-fund numbers. Recognition in the ecosystem can be a more significant indicator of future success than immediate performance data.

Advice for emerging managers

Ertan advises maintaining consistency, having a well-defined market thesis, and resisting the urge to significantly upscale the fund size or pivot strategies to follow current hypes. Managers should focus on being recognised as experts in their specific focus areas, which is seen as vital in a competitive market.

Key learnings

Alignment with thematic mega trends

Stephan Heller emphasises the importance of aligning with AQVC’s identified mega trends, ensuring that the emerging managers they consider investing in are working within these long-term trends and not short-term hypes.

Portfolio construction and geographical fit

AQVC seeks to avoid overlap with their current investments, meaning a new fund manager must offer something different either in terms of thesis or geographic focus.

Uniqueness and expertise

There is a significant focus on the uniqueness of a fund’s thesis and strategy, with a preference for those that truly understand their sector, such as climate tech, rather than simply following a trend.

Hustler mentality and long-term commitment

Stephan highlights the necessity for fund managers to possess a hustler mentality and a long-term view, underscoring that venture investments often take longer to mature than the average marriage.

Firm-building vision

AQVC is interested in managers with the vision to build a lasting firm, not just a one-time fund. This indicates a commitment to growth and evolution in the venture space.

Fund modeling and ownership

For first-time funds, Heller looks for evidence of strategic discipline, such as maintaining ownership percentages and leading or co-leading investments, as opposed to following big names into deals.

Appropriate fund sizing

Starting with a right-sized fund is crucial for new managers, with AQVC preferring those who demonstrate the discipline not to overextend on their first fund.

Execution on promises

For second-time funds, AQVC pays close attention to whether managers have executed on what they promised, both in terms of investments and firm-building efforts.

Liquidity creation capability

By the time a manager is raising a third fund, Heller expects to see some capability for liquidity creation, suggesting that successful fund managers should engage in intelligent capital velocity practices like partial secondaries or early M&A.

Deep due diligence with references

AQVC conducts thorough due diligence, including detailed reference checks, to validate track records and understand the real impact the manager had on successful deals.

For first-time managers without track record

Heller states that AQVC does not invest in first-time investors and suggests that aspiring managers build their track record within an existing VC firm.

Expectation management

For third-time funds, Stephan explains that while a 1x DPI towards the end of the fund’s life cycle would be acceptable, a complete lack of DPI might raise concerns, particularly if the underlying assets are heavily hyped with complex financial structures.

We also spoke to Rodrigo from Vinthera. Rodrigo brought a slightly different perspective, investing from a fund with a large co-investment component. So this conversation, naturally, focuses more on that (note: If co-investing with your LPs is top of your agenda, do make sure to also tune into this episode with Chris Wade from Isomer Capital and Alexis Hussou from HCVC which was fully dedicated to this topic.)

Key learnings

Three pillars of evaluation

Rodrigo emphasises three fundamental pillars in evaluating emerging managers: Strategy, Portfolio Construction, and Track Record. For Strategy, he looks at a fund’s USP (unique selling proposition) to founders, their access to quality deals, and the value they add to startups. Portfolio construction is key in understanding a fund’s dynamics, where Rodrigo appreciates a clear grasp of how ownership percentages and the size of the portfolio can significantly impact the fund’s potential success. Track Record is about more than just past performance; it encapsulates the team’s experience and the strategic fit with their venture thesis.

First-time firms, not first-time investors

Vinthera do invest in first-time firms, but not first-time investors. Rodrigo seeks evidence that prospective managers have achieved results, whether through operating experience, angel investing, or at a reputable venture firm. He values a history of making astute investments that show promise, even if not yet fully realised in financial terms.

Importance of portfolio construction

Understanding the mechanics of venture capital, such as the implications of ownership and follow-on investment strategies, is crucial. Rodrigo points out that a fund requiring many unicorns to succeed is less appealing than one where a single successful exit could return multiple times the fund’s value.

Concentration vs. diversification

Rodrigo notes that more concentrated portfolios may be better suited to seasoned industry professionals who can leverage their experience to make fewer, more impactful bets. Conversely, a diversified approach, with an initial broad portfolio followed by significant follow-ons in the most promising companies, can work well for firms that build strong relationships with founders and co-investors.

Co-investment strategy

In co-investments, the ability to move quickly and decisively is paramount. Vinthera’s structure allows for discretionary power over capital, enabling them to participate in rounds without delay. Building a solid, ongoing relationship with GPs ensures access to co-investment opportunities without the need for formal agreements.

Team assessment

Assessing an emerging manager’s team goes beyond the financials – it’s about understanding their motivations, their commitment to the industry, and what differentiates them in a crowded market. The “beer test,” as Rodrigo puts it, is an informal yet crucial part of this assessment – would he enjoy a casual conversation with this person outside of a business context?

Track record verification

For managers with previous experience, Rodrigo conducts thorough reference checks to validate their contributions to successful deals, ensuring that claimed achievements can be attributed to them.

Advice for emerging managers

Rodrigo’s advice is to build relationships with LPs when you’re not in fundraising mode, as this takes the transactional aspect out of the equation and fosters a genuine connection that can lead to better investment terms and stronger partnerships.

And finally, we did a roundtable on data-driven portfolio management, where demonstrating performance as a emerging manager was also central to the discussion. Check out the perspectives from Jon Coker at Eka VC, Joel Larsson at Pale Blue Dot, Joe Schorge from Isomer Capital and Anubhav the founder of Tactyc.

Key learnings

Advanced metrics usage

Emerging managers should be aware of various metrics, such as total portfolio revenue, cash, and burn rate. These figures provide a snapshot of the portfolio’s overall health and potential for growth, which is then weighted by the ownership percentage to simulate the “revenue of the fund.”

Capital efficiency consideration

A company’s capital efficiency is a vital metric, as it may not be reflected in traditional valuations between funding rounds. For instance, a company that hasn’t raised funds recently because it’s profitable and growing can be undervalued in a fund’s metrics.

Analyzing the investment lifecycle

Breaking down the MOIUC (multiple on invested capital) based on the timeframe and nature of investment (initial vs. follow-on) can offer insights into the fund manager’s abilities in both picking initial investments and managing ongoing deals.

Predicting winners is premature

It’s often too early to predict the portfolio’s winners, especially when the fund hasn’t finished investing. Ensuring that prospective as well as existing LPs understand and acknowledge the volatility and fragility of startups is important to ensure a context-aware evaluation of your performance.

Pacing analysis

Tracking and showcasing how a fund’s investments align with its original timeline and comparing the forecasted and actual capital deployment helps in deciding the optimal timing for raising subsequent funds as well as building the narrative accordingly.

Communication is key

How emerging managers communicate their fund’s performance to LPs is crucial. It’s often less about presenting specific numbers and more about articulating an understanding of the portfolio’s direction and the rationale behind it.

Qualitative over quantitative

The conversation around fund performance can often benefit from being made more qualitative, focusing on the narrative and potential of certain portfolio companies.

Minimize surprises

Large, unforeseen changes, like a star company you’ve consistently spoken highly of suddenly dropping to zero value, are unsettling for LPs. A good practice is to manage expectations by discussing both concerns and points of optimism when discussing individual portfolio companies.

LPs seek assurance

LPs are primarily interested in knowing that the GP is on top of the fund’s performance and that there is a system in place for monitoring and supporting portfolio companies, making it integral that you can engage in deep meaningful conversations about this.

Register to read more

Please fill in the form to access the full report.